📈 first Derivative [79]

March 17, 2023

Some news that bolsters the speculation that it was the US or allies behind the Nord Stream attacks, following up on fD[78]. Also some reasons why it would be Russia. Matt Stoller endorses the American Affairs essay about financialization and coordination (by fD reader Marc Rohatyn) that was in fD[77].

For those of you who tuned into the Oscars this year, Everything Everywhere All at Once swept the awards, including Best Picture. A huge night for A24 and for Asian-American representation on the screen. Personally, I liked, but didn’t love, EEAOO and my favorite movie of the year was Tár. Justin Chang wrote a nice piece in the Los Angeles Times post-Oscars that I think exactly captures how I feel about it (thanks to Gabriel for sending).

Happy reading :)

(If you have trouble reading Financial Times articles, email me)

-TK

🏦💻📈 Silicon Valley Bank goes under after a bank run. SVB was the 16th largest bank in the US with over $200B in assets and a key banking institution in venture capital and private equity. (FT | Tabby Kinder, Antoine Gara, Joshua Franklin, George Hammond | Mar 2023)

Basically, as I understand it, what happened was that in 2021 as private funding of companies ballooned, SVB, as the banking partner of choice, took in a lot of deposits. For banks, deposits are liabilities because the depositor can withdraw at any time and the bank has to produce the money. SVB had to decide what to do with all that money and:

searching for yield in an era of ultra-low interest rates, it ramped up investment in a $120bn portfolio of highly rated government-backed securities, $91bn of these in fixed-rate mortgage bonds carrying an average interest rate of just 1.64 per cent. While slightly higher than the meagre returns it could earn from short-term government debt, the investments locked the cash away for more than a decade and exposed it to losses if interest rates rose quickly.

Well, rates did rise (meaning bond values fell) and SVB’s bonds lost a lot of value, about $15B, which was almost equal to SVB’s total capital. Some of SVB’s bonds were categorized as “available for sale” meaning their value was marked as changing from quarter to quarter while others were classified as “held to maturity”, meaning that even though equivalent assets were trading at much lower prices, these assets were held on the bank’s balance sheet at cost because the bank intended to hold them until it could get its full principal back.

The problem was that SVB’s deposits kept dropping as the tech funding bubble popped and SVB needed to sell its bonds to meet those outflows. And when they sold the bonds they needed to mark them down in value.

Becker and his finance team decided to liquidate almost all of the bank’s “available for sale” securities portfolio and to reinvest the proceeds in shorter-term assets that would earn higher interest rates and improve the pressure on its profitability. The sale meant taking a $1.8bn hit, as the value of the securities had fallen since SVB had purchased them due to surging interest rates.

There was an attempt to raise capital but:

Rival bankers argued the plan was flawed from the outset — disclosing a $1.8bn loss at the same time as only securing $500mn of the $2.25bn capital raise from an anchor investor. “You can’t build a book while the market is open and you’re telling people there’s a $2bn hole,” said one senior banker at a competitor.

Ultimately the deal fell through when SVB’s stock price kept falling as more and more people were starting to become aware of the risk. Key VCs started encouraging their portfolio companies to withdraw their money, worsening the situation and starting the bank run that brought SVB down.

“They went for an extra [0.4 percentage points] of yield and blew up the bank,” said the person, whose fund held a bet against SVB. “It is really sad.”

Over the weekend this happened, there was a ton of uncertainty over whether or not the government would step in to guarantee deposits over the $250k per account threshold already insured by the FDIC. There was speculation that doing so would pose a moral hazard and that the haircut depositors would need to take would ultimately be small and tolerable. As for liquidity, secondary markets for SVB deposit claims seemed to spring up overnight. Others argued that SVB was a significant risk and would cripple the tech sector, specifically startups, many of which had all of their cash in SVB and wouldn’t be able to meet next payroll. Ultimately the government decided to guarantee all deposits at SVB as well as deposits at another bank, Signature Bank, and set up a liquidity facility to restore financial stability and confidence in several other regional banks that could be next if people started feeling unsafe about putting their money in any bank outside of the big 4 (Bank of America, Chase, Wells Fargo, Citi).

A lot of interesting angles to this story that is still playing out:

Will other banks with similar duration risk exposures fall leading to a banking crisis?

What are the unexpected knock-on effects of SVB’s collapse that will reverberate not just here in the US but overseas?

Will this lead to even greater concentration in the banking industry so that we end up with *only* banks that are too big to fail?

Why was the regulator in charge of SVB, the Fed specifically the SF Fed, not able to step in before we reached this point?

Should the rollback of regulations that were put in place post-financial crisis itself be rolled back?

Does the government now, explicitly or implicitly, back *all* bank deposits in the US? As of now, seems like they are trying not to give this impression

Should ordinary Americans be able to bank directly with the Federal Reserve or through some other national banking system similar to what’s available in other countries?

How do we deal with the moral hazard of once again socializing the losses from private businesses while the people who took these risks were able to, at least for a time, reap all the rewards? There’s definitely been attention on the hypocrisy of certain notable SV types, especially of the libertarian persuasion, calling for a government bailout while decrying similar largesse in other situations.

I’m still doing my reading as the situation keeps developing rapidly. But some interesting opinions on the issues I’ve come across:

Matt Stoller explains why the Fed was asleep at the wheel and argues we should end central bank independence. As people debate now whether this is technically a “bailout” or not, Stoller also goes over exactly what the policy response was and how it should be characterized. Sebastian Mallaby argues that SVB was not a systemic risk and should not have been bailed out: “Zero depositor losses equate to zero discipline on bankers. Henceforth, the only guarantee of sound behavior will be sound regulation.” It’s worth noting that SVB was giving out sweet deals for personal banking like below-market-rate mortgages for founders, in exchange for company money being kept at SVB.

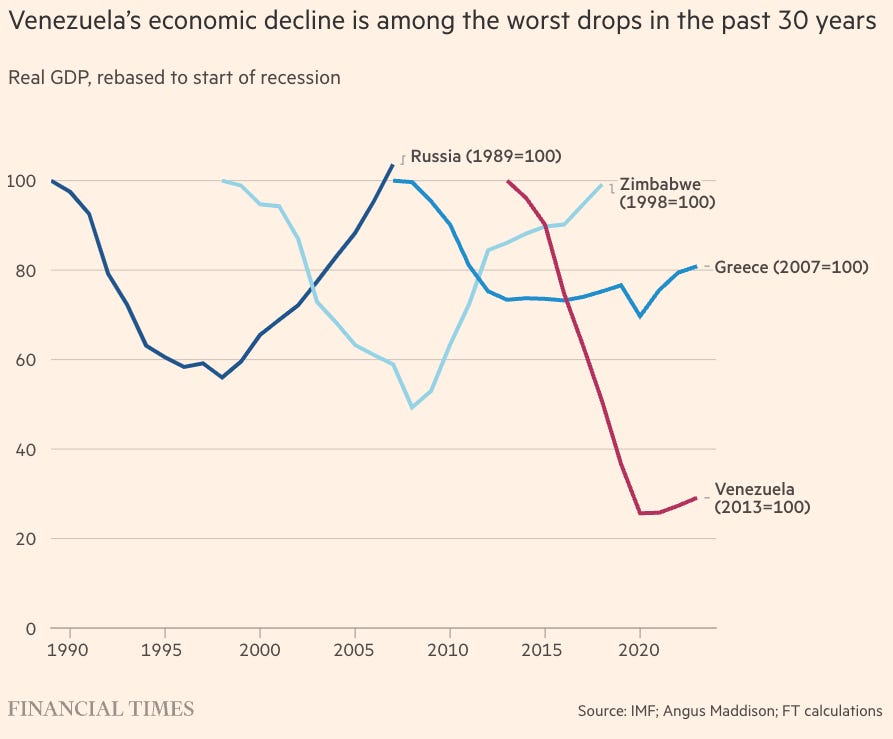

🇻🇪🛢📉 Venezuela’s economic decline under Maduro has been the worst of the past 30 years. Shrunk 70% in real terms. (FT | Michael Stott, Joe Daniels, Vanessa Silva | Mar 2023)

It’s not like I thought Venezuela was doing well but I had no idea it was this bad.

🏙🏗 Hit with the double whammy of higher interest rates and a remote/hybrid work landscape, the status quo in commercial real estate is becoming untenable both financially and municipally. Declining office building values are hitting city budgets. Developers are slowly starting to convert office buildings into residential. But the “office apocalypse” might be a “new opportunity for growth” and to combat the rising cost of housing. (WSJ | Peter Grant | Dec 2022) (FT | Joshua Chaffin | Feb 2023) (City Journal | Eric Kober | Winter 2023)

In jurisdictions that reassess property values annually, owner appeals of tax assessments are up 30% to 40% compared with a typical year before the pandemic, said Bryan Frey, a managing director in the valuation consulting business of CBRE Group Inc…

The prospect of reduced property taxes could also have implications for the $4 trillion U.S. municipal bond market. Merritt Research Services, a muni bond research firm, warned early in February that some major cities may be particularly vulnerable to office building re-evaluations because at least 8% of their tax base valuation is concentrated in their 10 largest commercial property taxpayers. This list includes Boston, Detroit and Denver, the report said.

S, an fD reader in real estate agrees: “cities with major exposure to office properties are going to lose considerable portions of their assessed value tax base if they sit idly…”

I just saw last month that Brookfield defaulted on loans backing two of its office buildings here in DTLA and they’re not the only ones. S: “one interesting part of these defaults that are happening now and more that will be coming is whether it’s true asset underperformance or whether it’s financial institutions playing finance games, strategically trying to get lenders to come to the negotiating table… there are many institutions who lend money who aren’t necessarily savvy real estate operators. And even if the lender is capable, many will not willingly take ownership of office assets at this point in time.”

If many firms really can run productively without a five-day-a-week employee presence in the office, that will represent a wrenching structural change in the economy—comparable with the post–World War II shift in manufacturing and goods distribution out of cities to peripheral locations in metropolitan areas, low-cost Sunbelt states, and low-wage foreign countries.

Really curious to see how the CRE situation plays out in major cities. Too optimistic to think this will help make cities more affordable again?

Housing prices and rents have subsequently risen much faster than incomes, effectively “pricing out” many people who want to move there. The need to recover tax revenues lost from declining office-space values creates a perfect excuse to unblock housing supply. New residents would ignite a demand for expanding services employment, as well as increasing the labor force, enabling expanding service businesses to help fill vacant offices.

If you’re interested, the FT article also has a lot of interesting little details about how office-to-residential conversions work and the headaches involved: elevators, floor layouts, windows.

🇲🇽🗳 Mexico Hobbles Election Agency That Helped End One-Party Rule (NYT | Natalie Kitroeff | Feb 2022)

Mexican lawmakers passed sweeping measures overhauling the nation’s electoral agency on Wednesday, dealing a blow to the institution that oversees voting and that helped push the country away from one-party rule two decades ago…

The watchdog, called the National Electoral Institute, earned international acclaim for facilitating clean elections in Mexico, paving the way for the opposition to win the presidency in 2000 after decades of rule by a single party.

Yet since losing a presidential election in 2006 by less than 1 percent of the vote, Mr. López Obrador has repeatedly argued, without evidence, that the watchdog actually perpetrated electoral fraud — a claim that resembles voter-fraud conspiracy theories in the United States and Brazil.

🚀🛠🤠 Elon Musk is building a town in Texas for his employees. (WSJ | Kirsten Grind, Rebecca Elliott, Ted Mann, Julie Bykowicz | Mar 2023)

Elon Musk is planning to build his own town on part of thousands of acres of newly purchased pasture and farmland outside the Texas capital, according to deeds and other land records and people familiar with the project.

In meetings with landowners and real-estate agents, Mr. Musk and employees of his companies have described his vision as a sort of Texas utopia along the Colorado River, where his employees could live and work.

Good job! Keep up the good work. Best,Bart